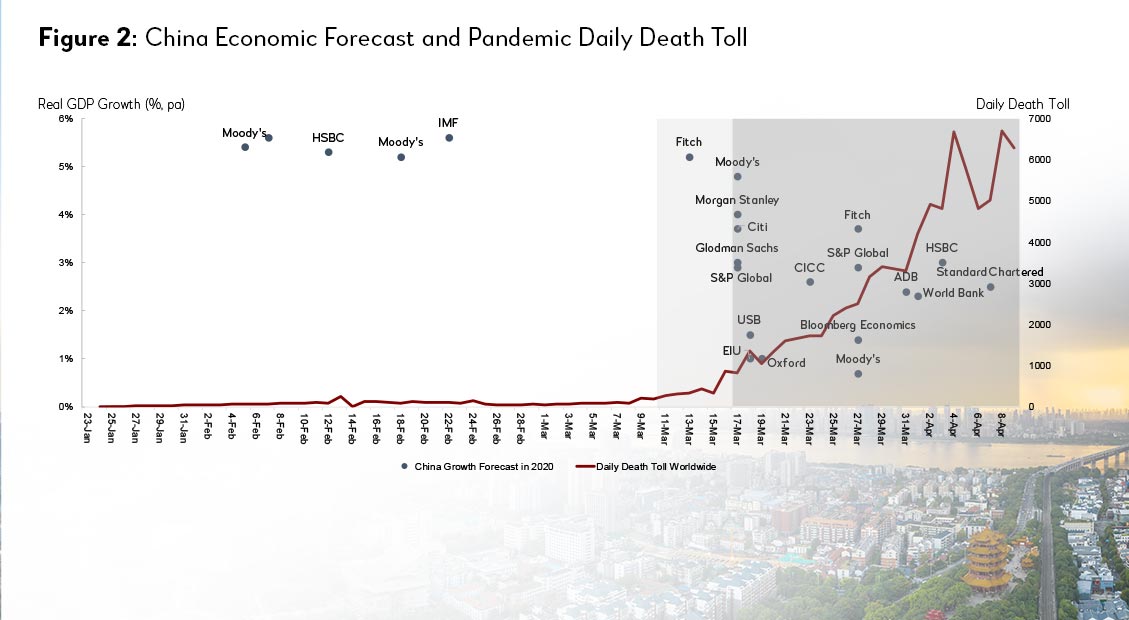

Since the Jan. 23, 2020 Wuhan lockdown, financial institutions have been assessing COVID-19’s impact and revising their forecasts on China. A sharp downturn in Q1 2020 (with a high possibility of extending to Q2) and an economic rebound in the second half was foreseen. Some sectors are showing signs of recovery in Q2.

Many more have died since COVID-19 became a pandemic on March 11, and the International Monetary Fund warned of “a recession at least as bad as the Global Financial Crisis.”1 Forecasts on China were further affected by global supply chain disruptions and the negative global economic outlook. After March 16, a day dubbed “another Black Monday,”2 China’s 2020 average growth forecast declined from 5 to 2.6 percent.

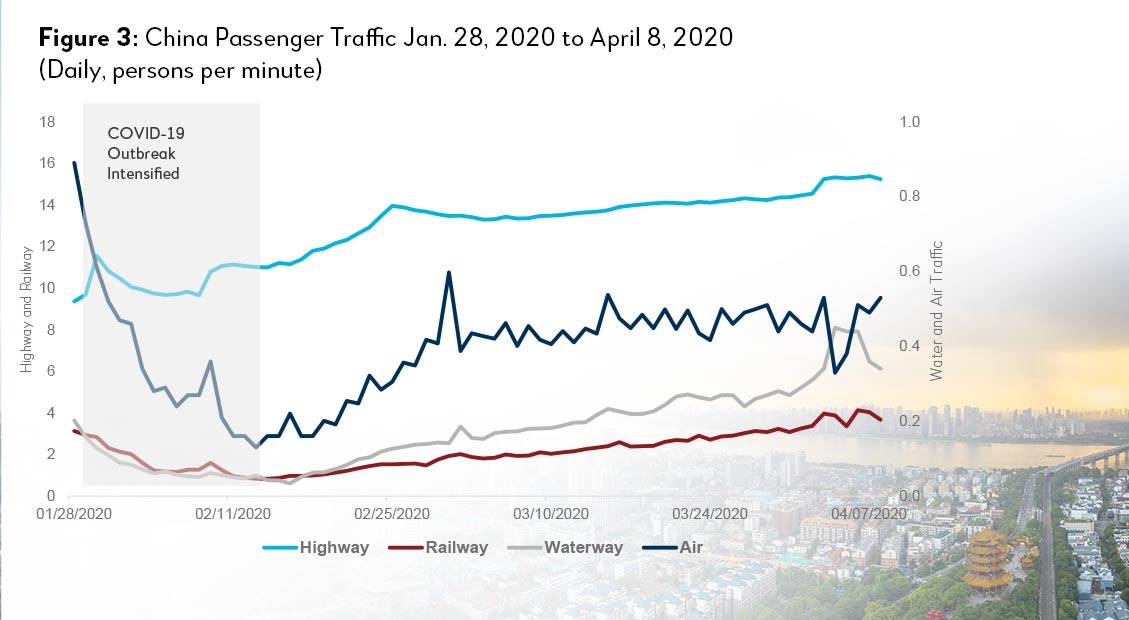

China encouraged less-affected sectors and manufacturing-heavy provinces to get “back to work,” and areas outside Hubei lifted traffic restrictions.3 China reported that 71.7 percent of small and medium-sized businesses resumed normal operations on March 24.4

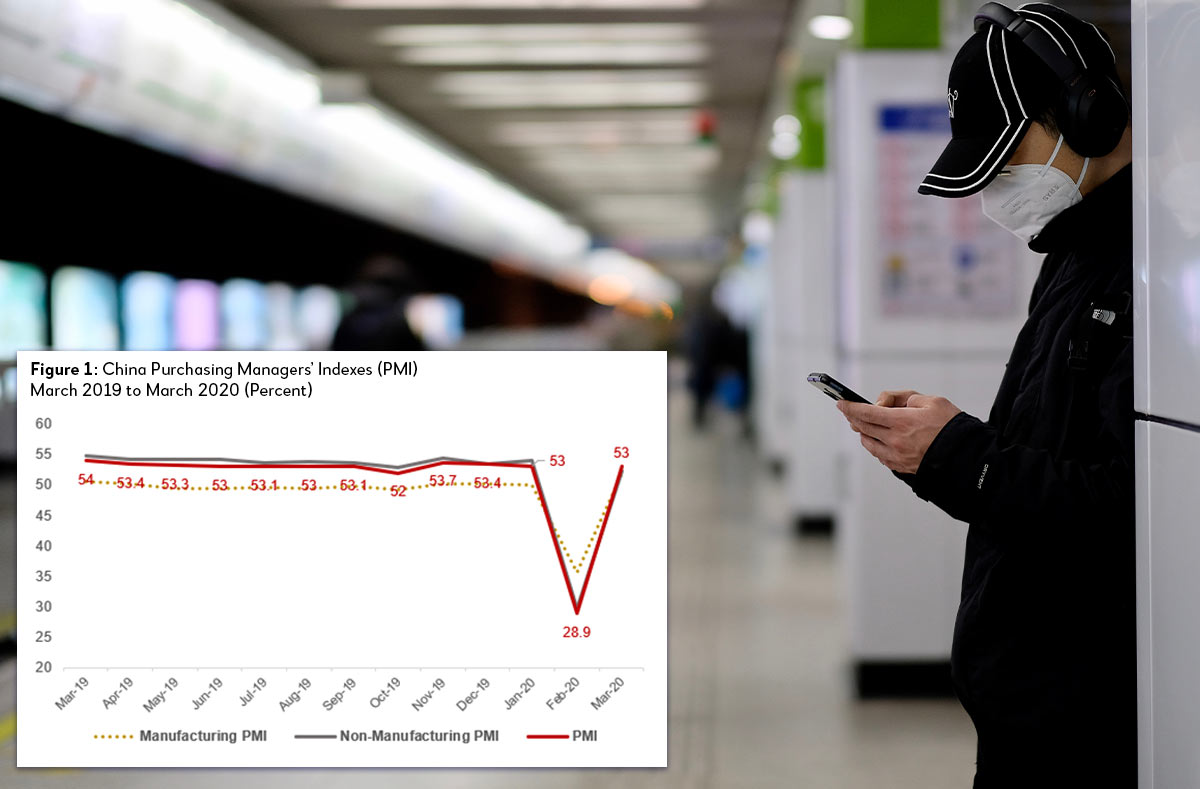

As provinces gradually resumed work, various sectors saw positive signs. Passenger traffic increased since the second week of February. The latest March Purchasing Managers’ Indexes (PMI) rebounded to above 50 percent after plunging below 30 percent in February. These suggest stabilization of domestic production activities.

However, some services face longer disruptions (restaurants, tourism and sports) where infection risks are high due to people gathering in confined spaces. Recovery rate in tourism and entertainment is thus lower than in manufacturing. As of March 22, only a third of tier-A national tourist sites5 and less than 5 percent of cinemas have returned to normal operations.6

To compensate for economic losses, some provinces plan to boost local tourism in Q2 with initiatives such as longer weekends, cash coupons and lower ticket prices.7 Other provinces might introduce stimulus packages for these sectors in the coming weeks. They will be especially important in today’s context when China’s economic recovery relies on domestic consumption. But even with supporting policies, the contribution of such sectors to the economy may be readjusted for a longer term.

The unprecedented lockdowns in China and other social distancing measures worldwide will impact how businesses, especially in the services industry, strive to remain as functional as possible during emergencies. Aside from policy incentives, resilient infrastructure—including efficient transport logistics, reliable digital connectivity and accessible social facilities—can help mitigate losses and facilitate recovery.

There are concerns over the agricultural sector as food production suspension and transport logistics disruptions affect China’s food security. These factors may have aggravated food inflation in February nationwide, particularly in Hubei and for fresh meat which is reliant on efficient logistics. Soybean meal prices rose 9.7 percent in late March against mid-March (China is a soy bean importer).8 External factors—such as threats from pests like desert locusts and fall armyworms, and food export restrictions in other countries—may further complicate efforts to maintain stable food prices.9

As the outbreak intensifies, countries may further restrict food exports to ensure domestic needs are prioritized. Preventing food prices from rising and mitigating the potential impact of such increases will likely be an imminent task for China in the short term.

China needs to watch the overall food situation as this could spread to the rest of the economy affected by COVID-19.10 In general, China is self-sufficient in terms of securing its basic food need. In 2018, over 95 percent of China’s cereals consumption was supplied domestically.11 For other economies where food supply is dependent on import and transport connectivity is underdeveloped, disruptions to domestic food supplies caused by COVID-19 will be more significant.

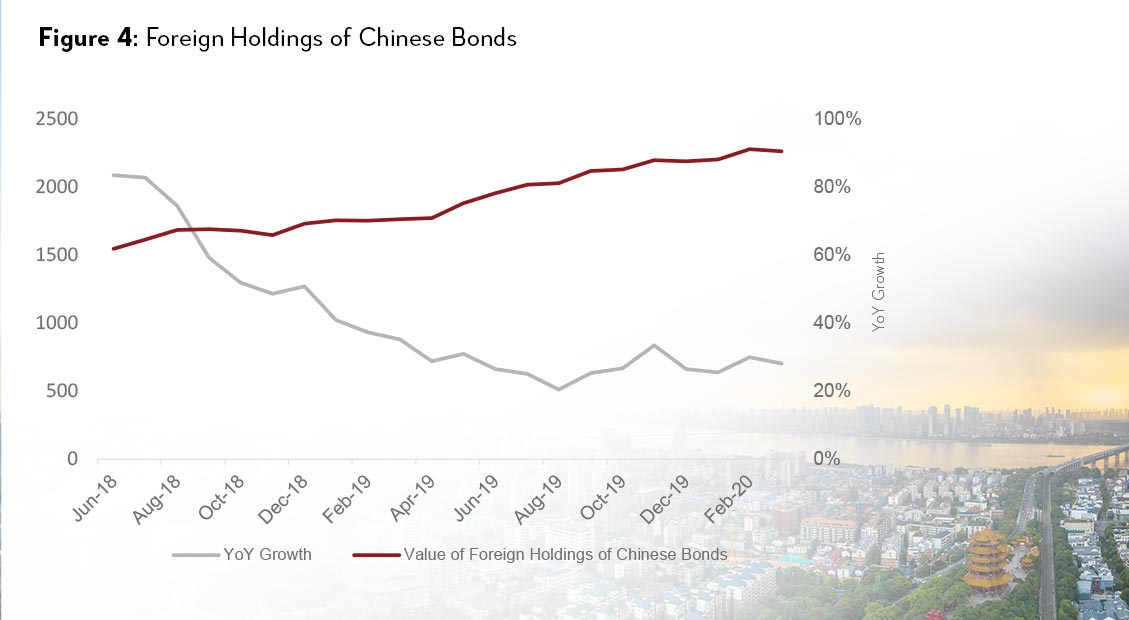

As of Feb. 29, 2020, offshore investors held RMB2.28 trillion (USD322 billion) in Chinese bonds, a record high.12 February foreign holdings of Chinese bonds saw a 30-percent year-on-year increase following a 25-percent increase in January. As central banks worldwide lower policy rates, interest rates in China (coupled with the reduced uncertainty as the spread of COVID-19 is curbed) made Chinese assets attractive to offshore investors. This resulted in yields on China’s 10-year government bond falling to 2.65 percent, lower than the 3.4 percent registered in the aftermath of the 2009 financial crisis and lower than the 3.2 percent observed in 2019. In Q1 2020, China’s corporates were also able to raise a record amount of cash (USD274 billion, up 26 percent compared with the same quarter in 2019) through bond issuances. The resilience of China’s bond and stock markets continued to point to China’s attractiveness to investors.

While some sectors are indeed showing promising signs, there is still uncertainty about the strength and durability of the recovery. Advanced economies are experiencing a “sudden stop” like China did in January and February. Moreover, with many precautions implemented, social distancing still in place and lower consumer sentiments, demand recovery will likely be sluggish after the initial burst following the easing of the toughest lockdown restrictions. China’s recovery is no doubt still hinged on the course of the pandemic. International cooperation to control COVID-19 and sustain global economic activity remains essential.

1 IMF Statement https://www.imf.org/en/News/Articles/2020/03/23/pr2098-imf-managing-director-statement-following-a-g20-ministerial-call-on-the-coronavirus-emergency.

2 Reuters https://www.reuters.com/article/us-usa-stocks/another-black-monday-as-coronavirus-response-upends-wall-street-idUSKBN2131B1.

3 Places classified as low risk can fully resume economic activities and remove traffic restrictions. Local authorities are also required to assist the affected enterprises to facilitate recovery. See: http://www.xinhuanet.com/politics/2020-02/25/c_1125625683.htm.

4 See news conference by the State Council on March 25: http://www.xinhuanet.com/politics/2020-03/26/c_1125768257.htm.

5 See news conference by the State Council on March 18. http://www.gov.cn/xinwen/gwylflkjz61/index.htm.

6 Recovery rate of cinemas reported by popular online film ticketing website Maoyan. http://www.chinanews.com/yl/2020/03-24/9135360.shtml.

7 On March 19 Jiangxi Province announced that it will encourage longer weekends and discounted tickets for all tier-A national parks in Q2. http://yuqing.people.com.cn/n1/2020/0320/c209043-31640960.html;.

Similar measures were also announced in Zhejiang Province. See http://www.chinanews.com/cj/2020/03-18/9130070.shtml.

8 National Bureau of Statistics, April 7, 2020: http://www.stats.gov.cn/tjsj/zxfb/202004/t20200407_1737098.html.

9 Pest control on fall armyworms (Spodoptera frugiperda), which can cause destructive damage to major cereal goods, is emphasized in the Ministry of Agriculture (MOA) policy priorities for 2020. See the policy document from MOA released on Feb. 6, 2020. On April 2, 2020, the central government passed new national administrative measures on pest control.

http://www.moa.gov.cn/ztzl/jj2020zyyhwj/2020zyyhwj/202002/t20200207_6336683.htm.

http://www.xinhuanet.com/politics/2020-04/02/c_1125806848.htm.

10 Laura Poppick. March 26, 2020. The Effects of COVID-19 Will Ripple through Food Systems. https://www.scientificamerican.com/article/the-effects-of-covid-19-will-ripple-through-food-systems.

11 White paper on Food Security in China released by the State Council in October 2019. http://www.gov.cn/zhengce/2019-10/14/content_5439410.htm.

12 Data released by China Central Depository and Clearing and Shanghai Clearing House.

DATA SOURCES: Figure 1: National Bureau of Statistics; Figure 2: WHO COVID-19 Situation Reports and Bloomberg; Figure 3: CEIC; Figure 4: CEIC.

{kind=link}